Bangladesh Bank’s decision to extend special policy support to the wilful defaulter-listed Krishibid Group—despite explicit prohibitions in its own regulations—has reignited debate over the central bank’s independence, internal decision-making, and the way power is exercised in the country’s financial system.

The episode also underscores a familiar pattern in the country’s political economy: powerful business groups, regardless of the government of the day, find ways to realign themselves—and ultimately secure favourable outcomes.

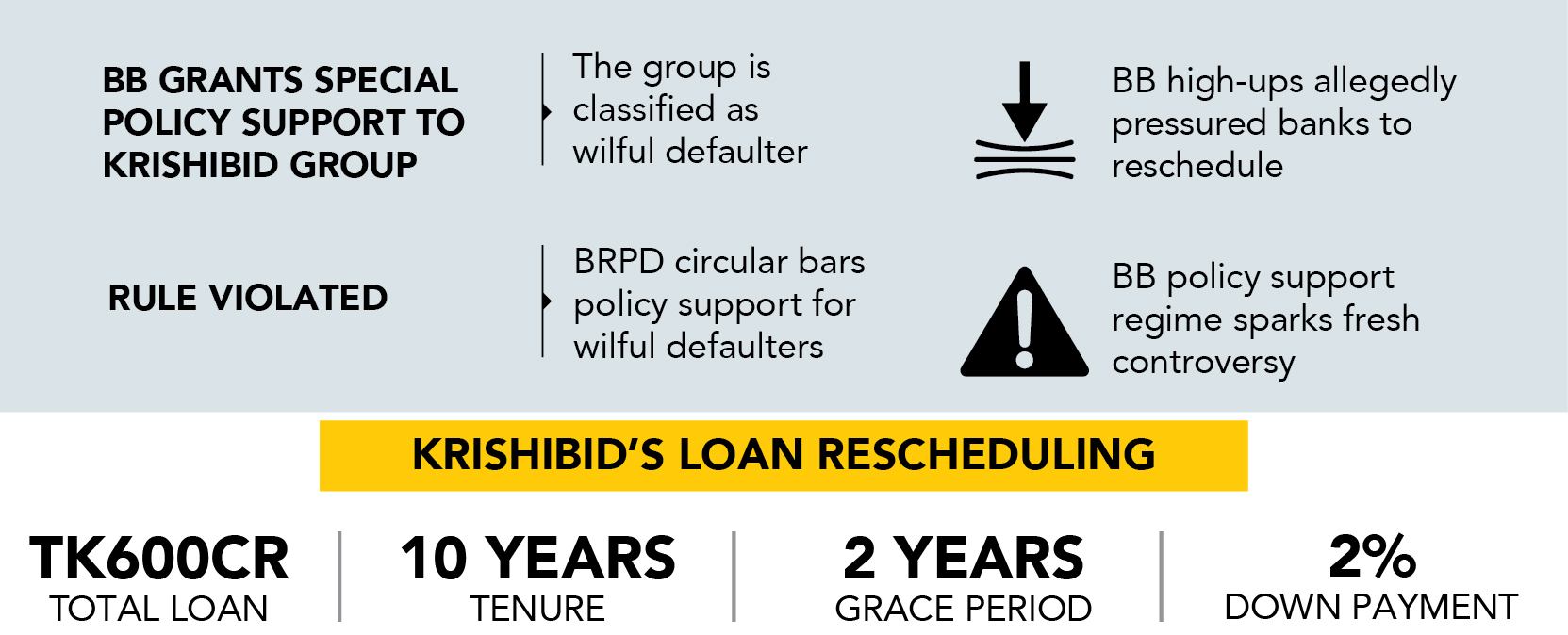

According to a Bangladesh Bank circular issued by its Banking Regulation and Policy Department (BRPD) on 16 September 2025, wilful defaulters are not eligible for any form of policy support.

Yet internal documents obtained by TIMES of Bangladesh show that the central bank instructed lenders to reschedule nearly Tk600 crore in loans taken by Krishibid Group over a 10-year period, including a two-year grace period. Banks were also told to withdraw the group’s wilful defaulter classification once a specified down payment was made.

The instructions, the letter says, were issued with the approval of Governor Ahsan H Mansur.

This has raised uncomfortable questions about regulatory credibility. By disregarding its own binding rules, the central bank sends a troubling signal to banks, borrowers, and the broader market about how selectively those rules may be applied.

The approval did not come easily. A policy support committee previously headed by former Executive Director Md Mezbaul Haque had rejected Krishibid Group’s application, citing ineligibility under the BRPD circular.

But after the group appealed, the committee was reconstituted under Executive Director Md Sirajul Islam. This new committee overturned the earlier decision and approved the special support.

Documents reviewed by TIMES confirm that final approval was granted at the committee’s 39th meeting on 23 September 2025. Following the governor’s consent, BRPD issued letters on 14 October instructing all lenders to implement the rescheduling.

Sirajul Islam later admitted to TIMES that the BRPD circular was not followed in this case. He said banks were instructed to withdraw the wilful defaulter classification after receiving the down payment.

This explanation directly contradicts the central bank’s own public stance.

Bangladesh Bank assistant spokesperson Mohammad Shahriar Siddiqui said, “If any borrower is classified as a wilful defaulter, there is no scope for policy support. Such facilities can only be extended after the wilful defaulter status is withdrawn.”

But Credit Information Bureau (CIB) records reviewed by this reporter show that as of 8 January this year, Krishibid Group was still listed as a wilful defaulter.

Under existing definitions, wilful defaulters are borrowers who obtained loans through fraud or deception, diverted funds, or refused to repay despite having the capacity to do so.

Despite this, Krishibid Group was offered unusually generous terms, including a down payment of just 2 percent—1 percent in cash and the remaining 1 percent payable after six months. The package also included a full two-year grace period with no instalments, followed by a repayment schedule allowing the remaining amount to be paid over 10 years.

For critics, this is not policy support—it is regulatory indulgence.

Internal sources allege that Bangladesh Bank officials did not stop at approving the package. They also pressured banks’ boards to implement the rescheduling.

Some banks reportedly resisted, citing the borrower’s wilful defaulter status. But they say they were leaned on.

Newly formed United Islamic Bank Chairman Mohammad Ayub Mia has also been accused of pressuring merged banks to approve the rescheduling. Multiple members of administration at Union Bank told TIMES that Mia phoned them repeatedly, urging them to comply.

One administrator claimed he called five times in a single day.

Mia denied the allegations, saying, “No special support or facility will be given to anyone beyond policy and rules.”

Bangladesh Bank had appointed administrators to five troubled Islamic banks last November—Union Bank, EXIM Bank, Social Islami Bank, Global Islami Bank and First Security Islami Bank—as part of a consolidation process. All administrators are central bank officials.

Krishibid Group has defaulted across eight banks and two financial institutions, including Al-Arafah Islami Bank, Islami Bank Bangladesh, Social Islami Bank, Shahjalal Islami Bank, Premier Bank, NRB Bank, Rupali Bank, IIDFC and IPDC Finance.

Documents show it remains classified as a wilful defaulter at Union Bank.

The group had already rescheduled its loans once in 2021 and 2022. Yet its businesses again failed to become regular. The October 2025 decision marked its second rescheduling.

The case has reignited criticism of Bangladesh Bank’s special policy support programme, originally launched to help businesses affected by political unrest, the pandemic, the Russia–Ukraine war, global recession and natural disasters.

In January last year, the central bank formed a five-member committee to oversee approvals. More than 1,600 applications were received, of which about 500 were approved.

From the outset, critics warned the programme could become a discretionary tool for favouritism. Bankers privately complained that politically connected borrowers were more likely to receive support.

Several managing directors told the governor that the programme was damaging banks’ liquidity and creating moral hazard—good borrowers were now demanding similar leniency.

In November 2025, Bangladesh Bank reversed course, issuing a circular transferring approval authority back to bank boards.

Agrani Bank chairman Syed Abu Naser Bukhtear Ahmed said, “The central bank should never be involved in approval processes. Its role should be supervision and oversight only. The moment it enters approvals, that is where the problems begin.”

Documents reveal that Krishibid Group founder and managing director Ali Afzal changed his political alignment after 5 August 2024—from being close to the Awami League to aligning with Jamaat-e-Islami.

He later sought a Jamaat nomination for the Magura-2 seat in the 13th parliamentary election but was denied due to his wilful defaulter status.

He is now reportedly keen to contest upcoming REHAB elections and has been actively seeking removal of the defaulter label.

Afzal told TIMES that he had been politically targeted under the previous government and unfairly declared a wilful defaulter.

“When Union Bank was under the control of the S Alam Group, they classified me as a wilful defaulter without prior notice,” he said. “There is a legal obligation to inform the borrower first.”

He claimed he only learned of the classification while applying for rescheduling last year.

He said Bangladesh Bank took these circumstances into account when granting policy support.