Agent banking in Bangladesh has reached a turning point. What began as a means of bringing banking services closer to people living far from branches has grown into a system that plays a central role.

At this scale, the key issue is no longer whether agent banking works. It is about how well the service can handle growing dependence along with rising risks and responsibility.

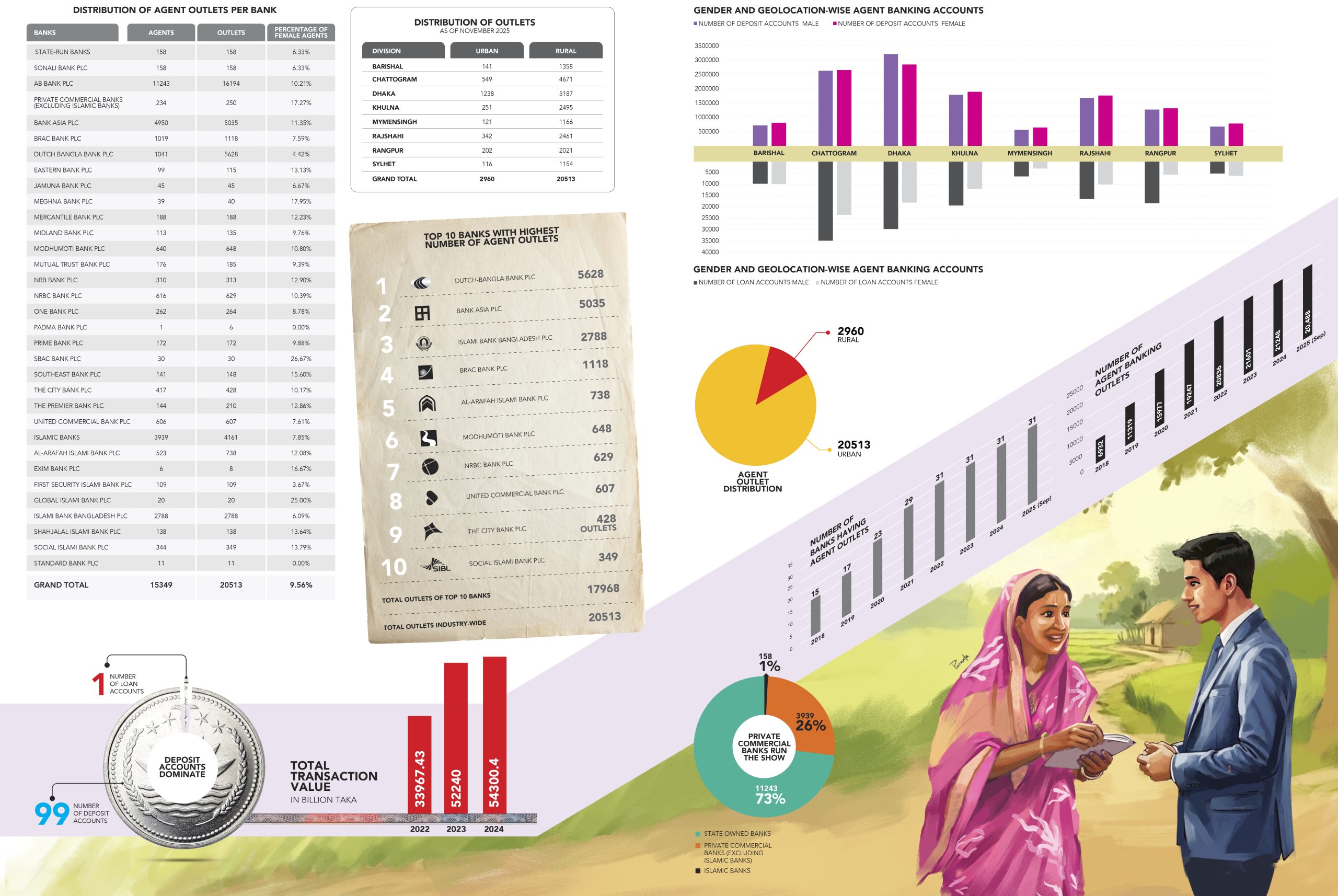

The growth has been rapid and far-reaching. In 2018, there were fewer than 7,000 agent banking outlets across the country.

By October 2025, there were 20,525 agent outlets bringing banking services into village markets, union centres and semi-urban areas where branches were never viable.

For millions of people, especially those living outside cities, local agent outlets have become the main place to deposit money, withdraw cash or receive remittance.

The number of customers tells a similar story. Deposit accounts made through agent banking grew from 2.45 million in 2018 to 25.62 million by November 2025.

This sharp rise shows how deeply agent banking has penetrated daily life. Many customers now rely entirely on agents for routine banking, rather than treating them as a secondary option.

Besides, savings have grown along with access. Deposit balances maintained through agent banking channels rose to Tk477.61 billion in November 2025 from Tk30.1 billion in 2018.

These balances may come from small, regular deposits, but together they represent a significant source of funds for banks.

Agent banking is no longer about tiny transactions alone. It now carries real financial weight. However, credit has not grown at the same pace. Loan disbursements through agent banking stood at just Tk314 million in 2018.

Although lending has expanded over the years, reaching about Tk62.1 billion by November 2025, it remains modest when set against the scale of deposits mobilised through this channel.

The contrast is striking; agent banking has become highly effective at collecting savings, but far less effective at returning those funds to rural and marginal customers in the form of credit.

Money is moving into the banking system through agents, but comparatively little is flowing back out as loans.

Transaction volumes underline just how important the system has become. In 2025, agent outlets handled 87.77 million transactions, up from around 82 million in 2022.

In terms of value, transactions reached Tk4.76 trillion (Tk476,000 crore) as of September last year, compared with Tk3.39 trillion (Tk339,000 crore) three years earlier. These figures show that agent banking now moves a large share of retail banking activity. In 2024, transactions amounted to Tk5.43 trillion.

This matters because agent banking is fully linked to banks’ core systems. Transactions at agent outlets are processed in real time and recorded directly in banks’ core banking platforms.

In practice, this means agent banking is already a part of core banking. When an agent outlet cannot operate, people in that area effectively lose access to basic banking services.

While access has expanded, new challenges have emerged. Agent banking is still affected by physical conditions at the local level. Cash shortages at outlets, power disruptions or network failures can stop transactions.

Control of agent banking networks has also become more concentrated. By 2025, 29 of the 31 banks offering agent banking services were private commercial banks. State-owned banks play a limited role.

Agent banking has brought banking services closer to people and helped millions enter the formal financial system. At the same time, its growing scale has created new risks and responsibilities.

How well these are managed will determine whether agent banking remains a lasting strength of Bangladesh’s financial system or becomes a source of pressure as its role continues to grow.