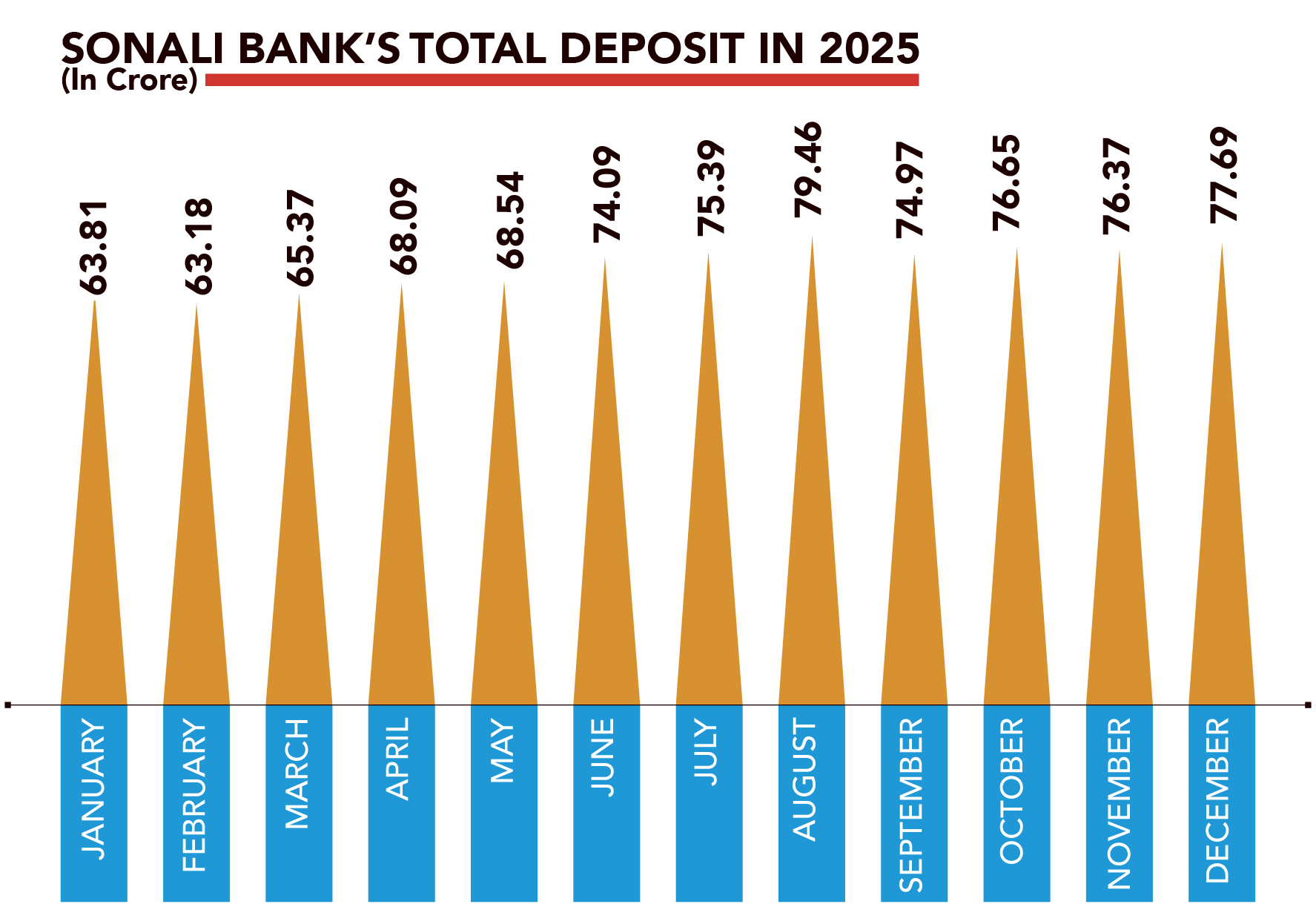

Sonali Bank’s agent banking programme shows how a state-owned lender is expanding access while keeping risks under control. Through around 227 active outlets, the bank handled Tk909.06 crore in transactions, mobilised Tk77.69 crore in deposits and earned Tk5.43 crore over the past year.

While loans are not yet offered through its agent outlets, the bank prioritises strict controls, biometric verification and internal oversight, with future growth focused on digital integration rather than rapid physical expansion. TIMES of Bangladesh Senior Staff Reporter Takie Mohammad Jubayer interviewed Sonali Bank PLC Managing Director and CEO Md Shawkat Ali Khan on the current state of agent banking and the bank’s plans. Here are excerpts from the interview.

TIMES: Agent banking is often seen as a promising model. Why did Sonali Bank choose to enter this space?

Shawkat Ali: Agent banking allows banks to reach people in remote and underserved areas without opening full branches. For Sonali Bank, it is a way to bring marginalised people into the formal banking system while keeping costs manageable. It also helps mobilise rural savings that would otherwise remain outside banks.

TIMES: Is agent banking expanding mainly for financial inclusion or because it costs less to operate?

Ali: Both reasons matter. Bangladesh Bank encourages agent banking to expand financial inclusion. At the same time, agent outlets are much cheaper to run than traditional branches, which makes the model practical for banks.

TIMES: How large is Sonali Bank’s agent banking operation now?

Ali: We currently operate through about 150 active agent outlets. In the past year, agent banking transactions amounted to Tk909 crore, while deposits reached Tk77.7 crore. The bank earned Tk5.43 crore from agent banking operations.

At this stage, we do not offer loans through agent outlets, but we are working to introduce lending in line with Bangladesh Bank guidelines and our internal policy.

TIMES: Many people say deposits are collected through agents, but little credit goes back to rural areas. Is that a concern?

Ali: I do not see agent banking as a system that drains rural savings. Instead, it helps bring marginalised people into the banking system and builds their financial capacity over time.

TIMES: What are the main risks involved in agent banking?

Ali: Like any financial service, agent banking involves risks. These include operational risk, money laundering risk, liquidity risk and reputational risk. These risks arise because transactions happen outside traditional branch settings.

TIMES: How does Sonali Bank control these risks?

Ali: We strictly follow Bangladesh Bank regulations and our own agent banking policy. All transactions require biometric verification. We use AML screening, monitor agent liquidity in real time and maintain clear systems for customer complaints.

TIMES: If an agent commits fraud or mishandles cash, who is responsible?

Ali: The bank is responsible. The agent works on behalf of the bank. If fraud happens at an authorised outlet, the bank must compensate the customer first and then take action against the agent.

TIMES: Have any customers been compensated for agent-related losses in the past year?

Ali: No. We have not faced such incidents. Our monitoring and audit systems have been strengthened to prevent this.

TIMES: Would you support allowing one agent to work for multiple banks?

Ali: No. That would increase risk, reduce job opportunities and create more chances for misconduct.

TIMES: Has regulation kept pace with the growth of agent banking?

Ali: That assessment rests with Bangladesh Bank as the regulator. The central bank is best placed to evaluate and respond to these developments.

TIMES: What is the most important reform needed to make agent banking sustainable?

Ali: Agent banking needs to move beyond basic cash services. Sustainability will come from linking agent outlets with digital banking so they can offer services such as insurance, mutual funds and small-value loans.

TIMES: What role has technology played so far?

Ali: Technology is central to our operations. Sonali Bank has completed its transition to real-time online banking through its core banking system, which improves efficiency and control.

TIMES: How do you see agent banking evolving in the next five to ten years?

Ali: Agent banking will continue to expand banking coverage in remote and underserved areas and remain an important part of Bangladesh’s financial system.