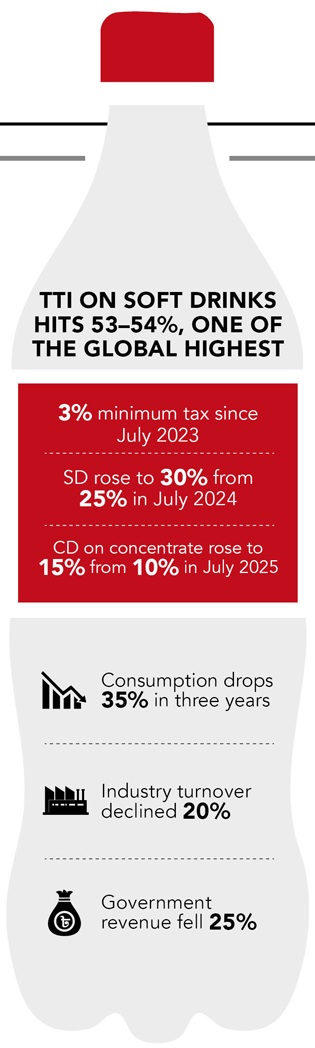

Government revenue from Bangladesh’s soft drinks sector fell 25 per cent in three fiscal years to Tk1,150 crore in FY2024–25 from Tk1,533 crore in FY2022–23, as successive tax hikes raised prices, reduced consumption by a third and shrank the market despite higher statutory rates.

The decline followed three consecutive tax increases by the National Board of Revenue.

Minimum tax on gross receipts rose fivefold to 3 per cent from 0.6 per cent in FY2023–24, supplementary duty increased to 30 per cent from 25 per cent in FY2024–25 and customs duty on beverage concentrate was raised to 15 per cent from 10 per cent in FY2025–26.

Combined with 15 per cent value-added tax, the total tax incidence (TTI) on carbonated beverages now stands at around 53–54 per cent, according to the industry, among the highest globally.

As a result, industry stakeholders said the cumulative burden sharply increased retail prices in a highly price-sensitive market where consumption remains among the world’s lowest.

Per capita soft drink consumption in Bangladesh stands at 8.4 glasses annually, while fewer than 5 per cent of consumers purchase soft drinks even once a year.

Soft drinks account for less than 0.05 per cent of total caloric intake, industry data show.

Moreover, according to Household Income and Expenditure Survey data from the Bangladesh Bureau of Statistics, single-serve beverages priced at Tk20–25 exceed the 6 per cent affordability threshold for daily fast-moving consumer goods spending.

Against this backdrop, the Bangladesh Beverage Manufacturers’ Association (BBMA), representing domestic and multinational producers, said repeated tax increases transformed the market from low consumption to structural demand contraction.

Industry estimates show the market size fell 20 per cent in three years to Tk8,000 crore from Tk10,000 crore, while total volume declined 35 per cent to 57 crore litres in FY2024–25 from 88 crore litres in FY2022–23 after falling to 63 crore litres in FY2023–24.

Manufacturers attributed the contraction to higher taxation alongside inflation, higher borrowing costs and nearly 40 per cent depreciation of the taka against the US dollar, which raised import-dependent raw material costs and weakened consumer purchasing power.

Meanwhile, Bangladesh’s overall tax incidence is significantly higher than regional peers, including around 40 per cent in India, 38.43 per cent in Nepal, 30 per cent in Bhutan and about 6 per cent in the Maldives. Industry sources said several Southeast Asian markets maintain overall tax incidence near 20 per cent.

Consequently, industry stakeholders warned the tax structure is also discouraging investment in one of the country’s major fast-moving consumer goods segments, which supports around 1.4 million direct and indirect jobs across manufacturing, logistics, retail and cold-chain infrastructure.

Bangladesh’s foreign direct investment-to-gross domestic product ratio remains below 1 per cent, compared with around 4.2 per cent in Vietnam. Stakeholders and foreign chambers said tax volatility and slowing consumption growth weakened reinvestment appetite among multinational companies, including within the Coca-Cola system.

In particular, the non-alcoholic ready-to-drink segment is considered strategically important for investment in packaging, transport and cold-chain infrastructure, though stakeholders warned policy uncertainty could delay future expansion by global operators including Anadolu Group.

At the same time, manufacturers criticised policy inconsistencies. While taxes on locally produced beverages increased, supplementary duty on imported ready-to-drink beverages was reduced by 50 per cent in FY2025–26. Industry players also noted supplementary duty on ice cream was lowered despite higher sugar content than soft drinks.

Stakeholders said higher domestic prices also encouraged illegal entry of foreign beverages and energy drinks, undermining compliant manufacturers and reducing formal tax collection.

Similarly, the Foreign Investors’ Chamber of Commerce and Industry and beverage manufacturers described the 500 per cent increase in minimum tax in FY2023–24 as disproportionate, arguing that it pushed products beyond consumer affordability and accelerated the fall in demand.

Manufacturers also opposed proposals to replace the existing ex-factory or value-added tax-based system with a maximum retail price-based tax structure, warning that the effective tax burden could rise to 75–78 per cent by taxing distributor and retailer margins not earned by producers.

According to industry stakeholders, such a shift could create cascading tax effects, force withdrawal of low-cost products and trigger further price inflation.

To ease pressure on the sector, the BBMA proposed reducing customs duty on beverage concentrate to 10 per cent from 15 per cent, lowering supplementary duty to 25 per cent from 30 per cent, cutting minimum tax to 1 per cent from 3 per cent, withdrawing supplementary duty on bottled water and retaining the existing ex-factory/value-added tax-based structure.

Ultimately, industry stakeholders argued that aligning Bangladesh’s tax regime with countries such as Thailand, Malaysia and Vietnam would improve affordability, revive consumption, encourage investment and increase long-term government revenue through higher sales volumes and broader compliance.